CONSULTING

Steel and automotive industry

Nikolas Alexander Scholz

Advisory consultant | Linkedin

This executive summary condenses the key findings of the report ‘Steel and Automotive Industry: Strategic Opportunities in a Transforming Ecosystem’. The study examines how electrification, vehicle lightweighting, and decarbonisation are reshaping material demand, cost structures, and strategic interactions between automotive OEMs and steel producers. It argues that the automotive sector can act as a catalyst for green steel adoption, while steelmakers can reposition from commodity suppliers to strategic partners offering high‑performance and low‑carbon solutions.

Steel in the global automotive industry

The automotive industry consumed roughly 209 million tonnes of finished steel in 2024, making it the third‑largest steel‑consuming sector globally after construction and infrastructure. Steel typically accounts for 50–65% of a passenger vehicle’s mass, owing to its strength, affordability, and versatility across structural and safety‑critical components. Although global vehicle production rebounded to 92.5 million units in 2024, the nature of automotive steel demand is evolving rapidly. Electrification, decarbonisation policies, and lightweighting strategies are driving a shift away from conventional mild steel toward advanced high‑strength steels (AHSS), ultra‑high‑strength steels (UHSS), aluminium, and low‑carbon steel. Regional dynamics shape this transition: China dominates absolute volumes but with lower steel intensity per vehicle, while Europe and Japan exhibit higher intensity and stronger regulatory pressure for sustainable materials. Given its scale and ability to absorb marginal cost increases, the automotive sector is uniquely positioned to anchor demand for low‑carbon steel and accelerate industry‑wide decarbonisation.

The automotive industry consumed roughly 209 million tonnes of finished steel in 2024, making it the third‑largest steel‑consuming sector globally after construction and infrastructure. Steel typically accounts for 50–65% of a passenger vehicle’s mass, owing to its strength, affordability, and versatility across structural and safety‑critical components. Although global vehicle production rebounded to 92.5 million units in 2024, the nature of automotive steel demand is evolving rapidly. Electrification, decarbonisation policies, and lightweighting strategies are driving a shift away from conventional mild steel toward advanced high‑strength steels (AHSS), ultra‑high‑strength steels (UHSS), aluminium, and low‑carbon steel. Regional dynamics shape this transition: China dominates absolute volumes but with lower steel intensity per vehicle, while Europe and Japan exhibit higher intensity and stronger regulatory pressure for sustainable materials. Given its scale and ability to absorb marginal cost increases, the automotive sector is uniquely positioned to anchor demand for low‑carbon steel and accelerate industry‑wide decarbonisation.

Lightweighting and the evolution of vehicle materials

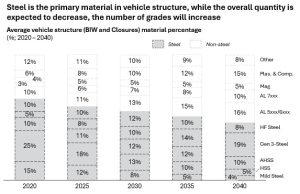

Over the past three decades, automakers have aggressively pursued lightweighting to improve fuel economy, extend EV range, and reduce emissions. The share of conventional steel in an average car has fallen from nearly 44% in the mid‑1990s to around 25% by 2020, replaced by aluminium, AHSS, plastics, and composites. Modern multi‑material vehicle designs can be 100–150 kg lighter than traditional all‑steel designs, delivering fuel‑economy improvements of 6–8% for internal combustion vehicles and offsetting battery mass in electric vehicles. Aluminium use has expanded rapidly, particularly in EVs, where aluminium content per vehicle now significantly exceeds that of gasoline cars. Despite these trends, steel remains indispensable due to its cost efficiency and safety performance, but its role is increasingly specialised. The strategic implication for steelmakers is a transition from bulk commodity volumes to value‑added, engineered grades tailored to specific automotive applications.

Notes: (1) 100% includes vehicle structure only which encompasses Body-in-White and Closures. Not included are powertrain/chassis, interiors, windshields and dynamic sealers. (2) 3rd Gen-Steel (AHSS) are multi-phase steels engineered to develop enhanced formability, have improved ductility in cold forming operations compared with other steels, according to World Auto Steel. (3) HF steel or Hot forming is a manufacturing process in which metal is heated above its recrystallization temperature to plastically deform it. This process allows the production of complex geometries while simultaneously enhancing the material properties. Source: Center for Automotive Research (CAR)

Electrification and new material dependencies

Electrification fundamentally restructures automotive material demand. Electric vehicles replace steel‑intensive combustion engines with battery packs and electric motors, increasing demand for copper, lithium, nickel, cobalt, graphite, and rare earth elements. Approximately 95% of EV motors use rare‑earth permanent magnets, driving exponential demand growth and exposing supply‑chain vulnerabilities. Rare earth mining and refining remain highly concentrated in China, creating strategic risks for Europe, the United States, and Japan. As a result, materials that were once commoditised inputs have become strategic assets. Automakers are increasingly embedding material strategy into product design and procurement, pursuing long‑term offtake agreements, equity investments in upstream assets, and R&D into material substitution and recycling. From a mining and metals perspective, electrification is turning niche materials into investable, system‑critical resources.

The green steel premium

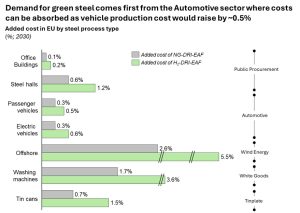

Source: “Transforming the Steel Industry May Be the Ultimate Climate Challenge” Notes: (1) Added cost assumes adding the cost of DRI-EAF (NG) or DRI-EAF (H2) compared to BF-BOF in 2030.

The green steel premium refers to the current cost differential between low‑carbon steel and conventional coal‑based BF‑BOF steel. Today, green steel produced via hydrogen‑based DRI or renewable‑powered EAF routes costs roughly 40–45% more than conventional steel. However, this premium has a limited impact on final vehicle prices because steel represents less than 10% of total manufacturing costs. Even a $400 per‑tonne steel premium typically raises the cost of a passenger car by around 1% or less. Multiple studies indicate that this premium will decline sharply as carbon pricing strengthens and clean‑energy technologies mature. Strategically, the green premium is not an economic barrier but a coordination challenge: aligning willingness to pay across the value chain. Early adopters can reduce Scope 3 emissions at minimal cost while enabling steelmakers to justify large‑scale investments in decarbonised production.

Emerging alliances between automakers and steelmakers

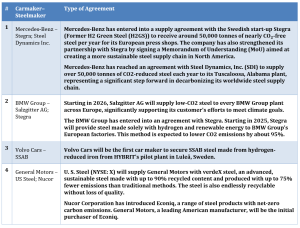

To overcome this coordination challenge, a growing wave of strategic alliances has emerged between automotive OEMs and steel producers. These include long‑term offtake agreements, memoranda of understanding, and early‑stage supply commitments for fossil‑free or low‑carbon steel. European automakers such as Mercedes‑Benz, BMW, Volvo, and Volkswagen have led these efforts, with U.S. and Japanese manufacturers increasingly following.

These partnerships provide steelmakers with demand certainty to de‑risk capital‑intensive hydrogen‑based projects while giving automakers early access to low‑carbon materials and a competitive sustainability advantage. Despite this momentum, current commitments still cover only a small fraction of automotive steel demand, highlighting the need for broader adoption to achieve material emissions reductions at scale.

Strategic opportunities for both sectors

The transformation of the automotive–steel ecosystem creates mutually reinforcing strategic opportunities. Automakers can differentiate through low‑carbon vehicles, secure critical material supply chains, and meet tightening regulatory requirements. Steelmakers can capture new value pools by scaling green steel, developing advanced grades, and repositioning themselves as collaborative partners rather than commodity suppliers.

Ultimately, success depends on coordinated action across the value chain: automakers providing credible demand signals and steel producers delivering competitive, decarbonised solutions. Together, these industries can build a resilient, innovative, and sustainable industrial ecosystem aligned with long‑term climate objectives.